Last week, a new Senate bill was introduced (by a bipartisan tandem of senators) to reauthorize the NFIP for 10 years, along with a study on flood insurance from the General Accounting Office (GAO). Both documents propose expansion of private flood insurance in the US. When added to the NAIC/CIPR’s flood study and the “monograph” (love that term) from the American Academy of Actuaries, the momentum in regulatory circles is clear. We just need something from The Big I to add to the choir.

The Senate bill, as mentioned, is intended to reauthorize the NFIP for another decade, but with significant changes. It does its best to juggle the various mandates the NFIP fulfills (flood plain management, flood risk mitigation, lender support, economic growth, along with flood insurance), and thus presents a bucket list of ambitions. As usual, the imperative on the NFIP to serve so many purposes will ultimately jeopardize its ability to be an effective insurer. However, as long as everyone is OK with this state of affairs and doesn’t expect the NFIP to actually be a solvent insurer of flood risk… whatever. Here is a link to Insurance Journal for a summarized version of the bucket list.

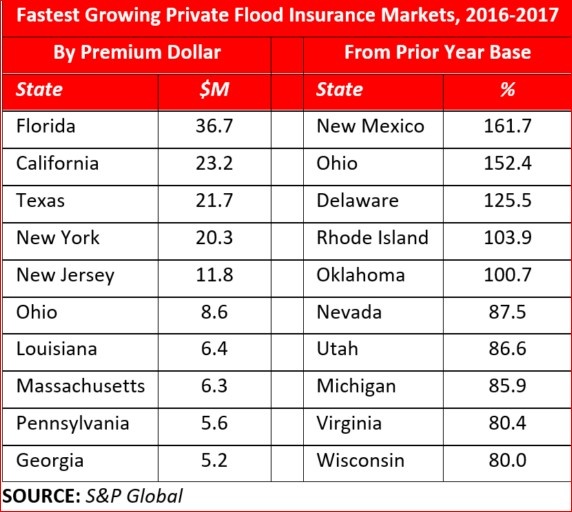

On the same day, the GAO released a study on flood insurance that complements the other studies coming out in April. It is a hefty affair, as one would expect from that august body of bureaucracy, but it is very, very good reading. The thing I like most about reading the GAO study is that it is the latest in a tradition of studies on flood insurance – they refer to their previous reports from decades past, often citing conclusions that have proven to be valid. The other studies are firmly focused on the present and future, while the GAO discusses the future from a durable and decades-long foundation of studies. And what do they say from this position? The same thing as everyone else: there needs to be more private flood insurance. Well, that’s one of their six conclusions, at least: